Updated July 2026

What Is Collision Coverage Insurance?

Collision coverage pays for damage to your vehicle when you collide with another car, a stationary object like a guardrail or tree, or roll your vehicle. It applies whether you caused the accident or someone else did, and it pays out even in single-vehicle accidents where no other driver is involved. The coverage pays up to your vehicle's actual cash value minus your chosen deductible, not the replacement cost or purchase price.

- You brake for debris on I-35 and slide into a concrete barrier. Your 2014 sedan sustains $5,200 in damage. Your liability-only policy pays nothing for your vehicle. With collision coverage and a $500 deductible, your insurer pays $4,700. Without collision, you pay the full $5,200 or drive a damaged vehicle.

- You misjudge a turn in a parking lot and scrape another parked car, causing $1,800 damage to their vehicle and $2,400 to yours. Your liability coverage pays the $1,800 for their car. Collision coverage pays the $2,400 for your vehicle minus your deductible. Without collision, their damage is covered but yours is not.

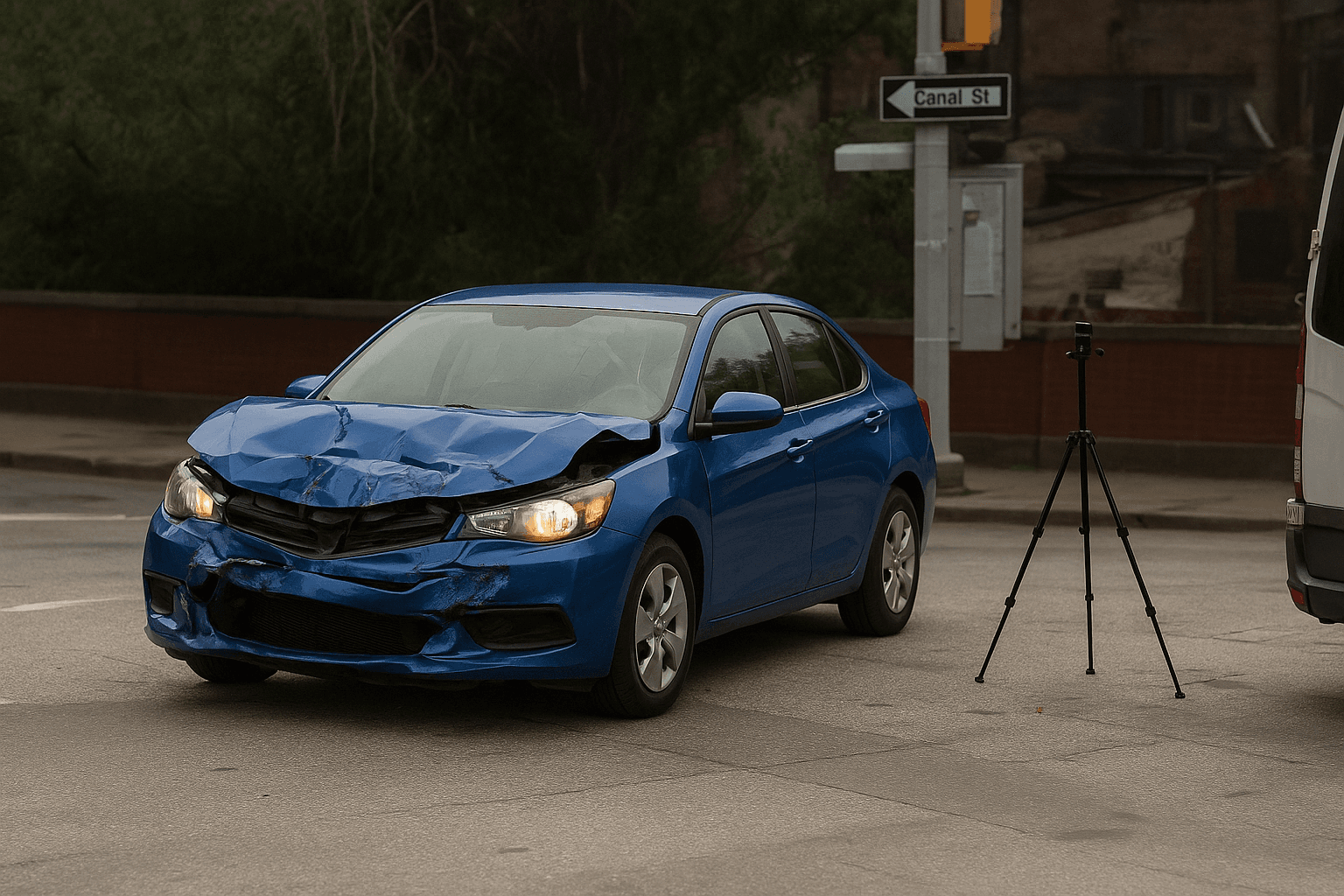

- An uninsured driver rear-ends you at a stoplight, causing $3,600 in damage to your vehicle. Uninsured motorist property damage coverage in Texas has a $250 deductible and pays up to $25,000. Collision coverage also pays, often with a higher deductible. You file under whichever coverage offers the lower out-of-pocket cost, but you need at least one of them — liability alone pays nothing for your vehicle.

Who Needs Collision Coverage Insurance?

Retirees driving vehicles worth more than $5,000 should keep collision coverage — the premium is justified by the replacement cost if you're at fault or hit by an uninsured driver. If you're still paying off a vehicle, your lender contractually requires collision until the loan is satisfied. Retirees who would struggle to replace a vehicle out-of-pocket benefit from collision even on older cars, as long as annual premiums stay below 15 percent of the vehicle's value.

Calculate your vehicle's actual cash value using Kelley Blue Book or NADA, not what you paid or what replacement would cost. Subtract your deductible from that value. If annual collision premiums exceed 15 percent of the net recovery amount, consider dropping collision and setting aside the premium savings in a vehicle replacement fund. Revisit the decision annually as vehicle value declines and premiums adjust.

How Much Does Collision Coverage Insurance Cost?

Collision coverage typically adds $30 to $85 per month for retirees with clean records driving paid-off vehicles in Texas, or $360 to $1,020 annually.

- Vehicle value — a 2010 Camry with $6,500 actual cash value costs less to insure for collision than a 2020 model worth $18,000.

- Deductible choice — raising your deductible from $500 to $1,000 can reduce collision premiums by 20 to 30 percent.

- Driving record — collision claims in the prior three years increase premiums significantly; a clean record qualifies for the lowest tier.

- Garaging location — collision costs more in Houston and Dallas due to higher accident frequency than in rural counties.

- Mileage — retirees driving under 7,500 miles annually often qualify for low-mileage discounts that reduce collision premiums by 10 to 20 percent with carriers like State Farm and Nationwide.

- Bundled discounts — combining collision with comprehensive and taking a mature-driver course can reduce the combined premium by 10 to 15 percent with carriers writing in Texas.